EPF Compliance

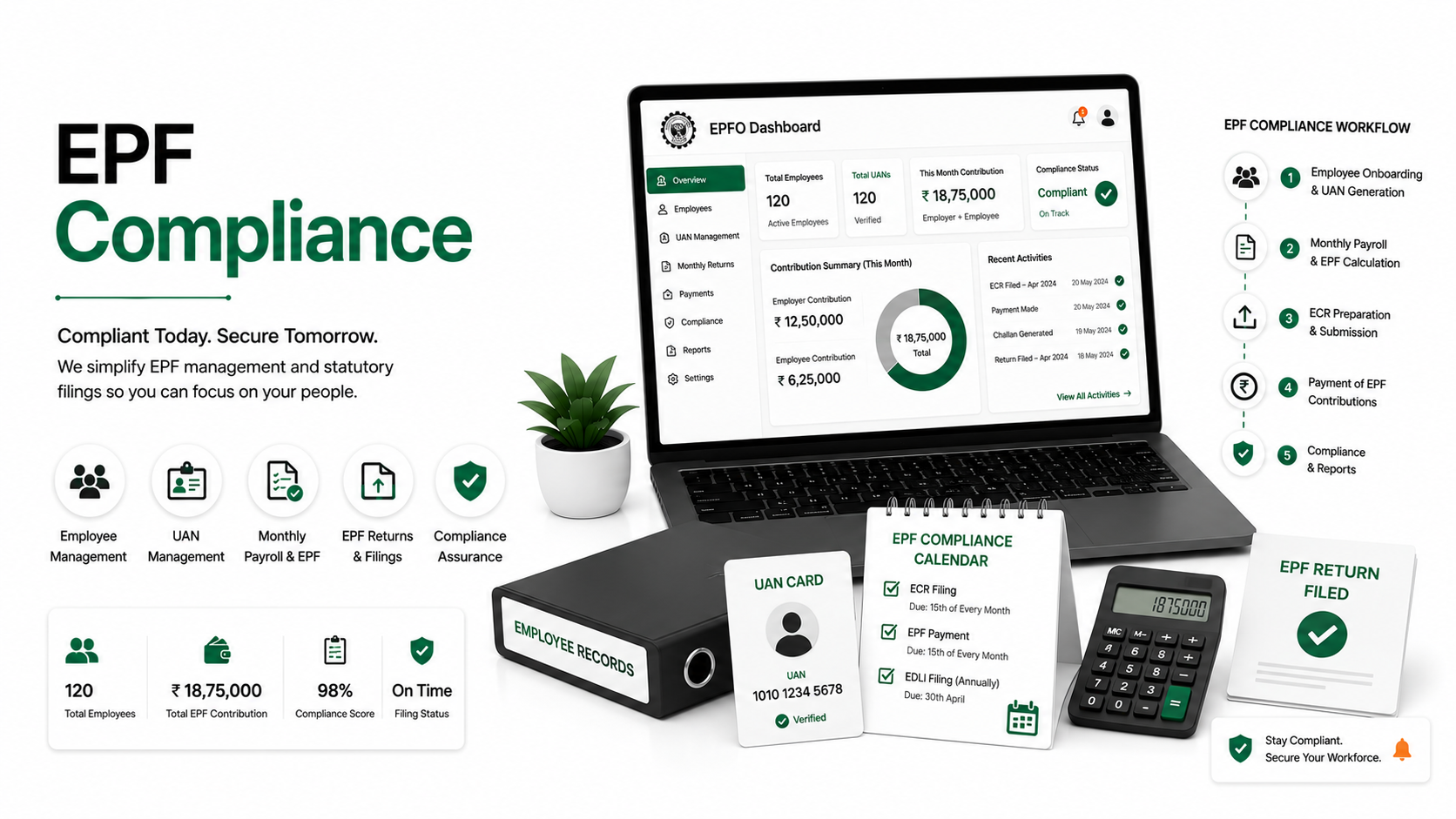

Employer registration, monthly ECR filing, UAN management and full EPFO compliance for covered establishments.

Everything a growing business needs.

- EPF establishment registration on the EPFO portal

- Monthly PF return filing (ECR — Electronic Challan cum Return)

- Employee enrolment on EPFO — UAN generation and KYC seeding

- PF challan calculation and payment before 15th of each month

- KYC approval for Aadhaar, PAN, and bank account on EPFO portal

- Assistance with PF withdrawal and transfer claims for employees

- EPFO inspection compliance and response to notices

The statutory frame we work in.

Questions we hear often.

At what employee strength does EPF become mandatory?

+

EPF is mandatory for establishments employing 20 or more employees. Once covered, coverage continues even if employee count falls below 20. Voluntary coverage is available for smaller establishments.

What is the Basic Wage for EPF computation?

+

PF contributions are calculated on "basic wages" which includes basic pay, dearness allowance, and retaining allowance but excludes HRA, overtime, bonuses, and commission. Structuring salary components incorrectly to reduce PF liability is a common compliance risk.

What happens if PF is not remitted on time?

+

Interest at 12% per annum applies on delayed deposits. In addition, damages under Section 14B can be levied at 5%–25% of the shortfall depending on the period of delay. Criminal prosecution is possible for continued default.

A first consultation is on us.

Tell us a little about your business. We'll come back within one business day with a fixed-fee quote and a short engagement scope.